Jewelry Industry: Branded jewelry leads the way in hard luxury, with major shifts underway

Jewelry Industry: Branded jewelry leads the way in hard luxury, with major shifts underway

The jewelry industry is undergoing a significant transformation. Historically characterized by its fragmentation, the market is witnessing a steady shift towards branding, much like what happened with luxury watches in previous decades. And just like what is happening in the luxury industry overall, the brands and iconic product lines are shifting into a virtuous circle of growth.

Despite this evolution, the landscape remains highly fragmented, with countless independent jewelers still competing alongside emerging and established brands. This dichotomy presents both challenges and opportunities in a market where consumer expectations, digital presence and brand storytelling are becoming increasingly pivotal.

A row of diamond dealers in Antwerp, Belgium

A jewelry store in the New York diamond district

A Shift Toward Branded Jewelry

In the past, jewelry was largely sold through local, independent retailers, with a focus on craftsmanship and heritage. But also, thanks to a lower entry ticket in terms of product technicalities, developing a distinctive design and bringing it to the market is a lot easier for jewels than it is for watches — at least in the upper end of the price segments.

Another market differentiator is the fact that you will find many more manufacturers offering private or white labeling services in the jewelry industry than you will find for watches. Again, this applies for the premium to luxury segments, because developing low- to mid-end watches is quite simple with the myriads of Asian watch component producers.

As a clear proof, we estimate that there are at least one to two new watch brands coming to the market every week. But in jewelry that number is a multiple; besides that, there are still many retailers around the world, especially in China, Italy or Germany having their jewelry produced by private label manufacturers. When you walk through the exhibition halls of the recent Vicenza Oro fair and you see the dozens of booths offering jewels and unbranded jewelry, you start understanding that the product offering is still huge.

However, in recent years, branded jewelry has gained considerable traction. Iconic names like Cartier, Bvlgari or Chopard have long dominated the luxury end of the market, but more contemporary brands, such as Messika and Pomellato, have started to attract a younger clientele.

Cartier's landmark Champs-Élysées store

Boucheron's signature Quatre jewelry collection

This growth in branding is largely fueled by two factors.

Changing Consumer Preferences

Even though there are divergent theories that Gen Z are a lot less into luxury consumption than experiences, they do value brands with a strong story of purpose. Modern consumers, particularly millennials and Gen Z, value brand recognition and often seek pieces that come with a story or ethos they resonate with. Branded jewelry offers a form of assurance about the product’s quality, ethical sourcing and craftsmanship, creating emotional connections that go beyond the intrinsic value of the materials.

Digital and Omnichannel Experience

Digital marketing has revolutionized how jewelry is perceived and sold. Online platforms and social media have allowed brands to engage with consumers more directly, often bypassing traditional retail channels. Here we find the parallels with the watch industry, where blogs and influencers — the latter with a recent loss of relevance though — implored that brands change their way of communicating with the end consumers.

Brands like Blue Nile (part of the Signet Group) and Brilliant Earth leverage this by offering personalized experiences and ethical sourcing information, which appeal to the values of a younger, more informed audience. Brilliant Earth communicates about all its efforts to make the jewelry value chain more sustainable and ethical by using the most recycled and Fairmined raw materials. Claiming to be using 96 percent of recycled gold, it reaches already a substantially higher rate than any watch brand, but at the same time, the manufacturing processes can’t be 100 percent compared.

The rise of e-commerce in jewelry has also contributed to the acceleration of branded players, as they adapt faster to new technologies and digital strategies than independent, traditional jewelers. On the other hand, newly launched niche players are managing to play a significant role if they manage to engage with a large and focused community. This can include crowdfunding and crowd creation by having the community co-decide on aesthetical choices for new products.

Fragmentation Persists

Despite this shift towards branded jewelry, the market remains highly fragmented. According to industry reports, approximately 80 percent (~83 percent estimated by Morgan Stanley based on Bain-Altagamma figures) of the global jewelry market is still composed of small, independent retailers or major unbranded suppliers, for instance in India. This contrasts sharply with the watch industry, where one dominant player such as Rolex captures 30 percent market share and where five brands take more than half of the Swiss watch market (~53 percent by estimate of Morgan Stanley ×LuxeConsult).

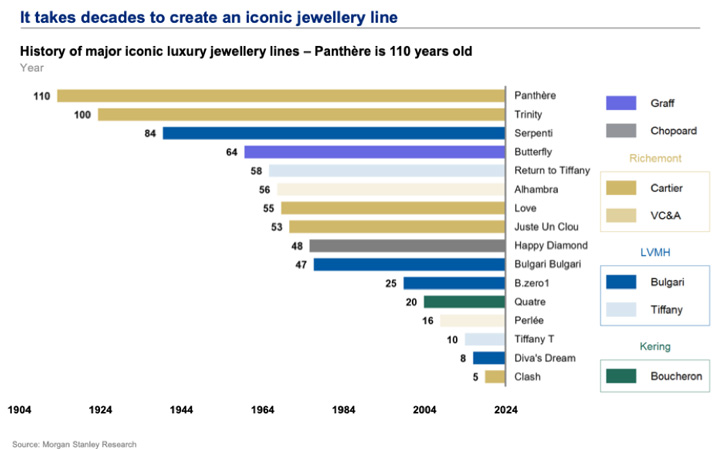

The dominant player is clearly Cartier which by coincidence captures also ~7 percent of the Swiss watch market but in second place and with only one quarter of Rolex’s market share. The common thread of Cartier’s strength on the two markets is its strong brand equity and the iconic product lines. Just like the watches of Cartier can boast to carry the oldest and strongest product icons, the Panthère jewelry line, like the Tank for the watches, is never out of fashion and a perpetually renewed product line. But the most impressive, in my opinion, is the fact that Cartier still manages to create new icons besides the Panthère and Trinity, which are more than a century old. The Clash, launched as recently as 2019, is already on track to become the new icon of the maison Cartier.

Luxury Groups Largely Dominate the Game

Unlike what is happening in the watch industry where privately owned brands — Rolex, Patek Philippe, Audemars Piguet and Richard Mille — grow faster than the ones owned by listed groups or brands, with the exception of Cartier (under the Richemont umbrella), groups master the game in the jewelry business. The first privately owned brand — Graff — comes “only” in fifth position of the luxury jewelry maisons, followed by another family owned brand, Chopard.

Nevertheless, huge investments are needed to reposition a brand, as the example of Tiffany is just showing, which is far from being a walk in the park for LVMH. Despite having invested massive amounts of money, hired the most iconic brand ambassadors and having totally transformed the historic flagship store in New York, the iconic brand is still struggling compared with its direct competitor Cartier. I would dare to predict that LVMH’s plan to push both on Bvlgari and Tiffany to challenge Richemont will eventually pay off, but unlike what the chairman of the group, Mr. Arnault, probably expects, it will take another few years if not a decade.

The following chart gives an overview on the ranking of the different players, but to be fair we should add that only the total sales of the brands are being compared. And in the case of Tiffany, for which watches account for only ~7 percent of the total sales, the comparison with Cartier changes quite dramatically if we estimate the jewelry sales to be at ~65 percent that would set the comparison at EUR 4.9 billion and EUR 6.9 billion, respectively.

Challenges for Independent Jewelers

For independent jewelers, this branded shift poses several challenges.

Brand Power or Brand Equity

Competing with the marketing budgets and brand recognition of global players is difficult. Independent jewelers often lack the resources to invest in sophisticated digital marketing strategies or influencer collaborations, leaving them at a disadvantage when trying to attract younger, brand-conscious consumers.

Supply Chain Constraints

Larger brands are better positioned to secure ethical and traceable supply chains, which are increasingly important to consumers. Smaller players may struggle to offer the same level of transparency, impacting their ability to compete on values like sustainability and ethical sourcing, even though one can argue that sustainability is not only about the raw materials, but also the global footprint that the brand will have to manufacture and deliver the products. There are artisan jewelers who are offering to create new jewels with old ones, yours or some that the artisan is buying at auctions for the purpose of recycling and upcycling them.

Evolving Consumer Behavior

The rise of digital-first brands means that consumers — especially Gen Z dubbed as “digital natives” — expect a seamless online-to-offline shopping experience. Independent retailers, often slower to adopt these trends, risk falling behind as they rely on traditional business models.

Opportunities in a Fragmented Market

Despite the challenges, there are also opportunities. The same consumer desire for personalization and ethical consumption that drives branded jewelry can also benefit independent jewelers and brands, provided they can adapt.

Niche and Customization

Independent jewelers have the advantage of flexibility and are able to offer more niche, bespoke or artisan pieces that branded players cannot replicate at scale. Customization and uniqueness will always have a place in the market, especially in an industry as personal as jewelry. And what is more characteristic of luxury than customization and handcraft? A strong brand might bring social recognition, but a niche and rare product might be a better reward for the younger generation.

Local Expertise and Heritage

Smaller retailers can capitalize on their history and local expertise. Highlighting heritage craftsmanship and offering more personalized customer service can differentiate them in an increasingly homogenized market. Those two — at first sight completely contradictory — market trends can be seen overall and not only in luxury. The mighty power of globalized brands is in fact the best breeding ground for niche brands, just as we see with artisan watch brands becoming the epitome of the new quest for something different than the institutional brands can offer.

Collaboration

The rise of branded jewelry does not have to come at the expense of smaller players. Some independent jewelers have found success collaborating with larger brands, or entering marketplaces that allow them to reach a broader audience without losing their artisanal identity.

The jewelry industry today stands at a crossroads. The rise of branded jewelry reflects broader consumer trends towards recognition, quality assurance and ethical consumption. Yet, the industry’s deep-rooted fragmentation persists, sustained by the enduring appeal of independent, bespoke craftsmanship. For both branded and independent players, the future lies in their ability to balance tradition with innovation, ensuring that they remain relevant in a rapidly evolving marketplace.

The jewelry industry may be on the brink of further consolidation, but its inherent diversity ensures that there will always be room for both global brands and local artisans. Those who can adapt their business models to incorporate the best of both worlds — branding, digital strategy and artisanal craftsmanship — are likely to thrive in this dynamic environment.